Last Updated on: Sep 01, 2022

The benefits of life insurance are well-established. Regardless of your age, the right policy can provide significant peace of mind, ensuring that your closest family is protected in the event of the unthinkable.

What We'll Cover

- The Factors that Play Into Your Recommended Life Insurance Amount

- How to Choose a Life Insurance Amount Based on Your Income

- How Your Family and Living Situation Play Into the Ideal Life Insurance Amount

- What is a Good Life Insurance Amount if I Have Debt?

- The DIME Method for Life Insurance Coverage

- 5 Considerations to Make Sure the Right Life Insurance Amount is Right For You

- Conclusion

But of course, understanding that you should get life insurance is only the beginning. The next decision is just as important: how do you know what a good life insurance amount is?

The answer is not necessarily simple. That's because, as it turns out, it depends on a variety of factors. So, instead of just answering a simple question like whether a 250k life insurance is enough, this guide will give you all the information you need to choose the right life insurance amount for your situation.

The Factors that Play Into Your Recommended Life Insurance Amount

Let's start with a basic overview of what exact factors tend to determine how most people choose the amount of their life insurance policy. We'll then dive into each of these in more detail below:

- Your current income

- Your current debts

- Your family and living situation

- Your standard of living

Each of the above play equal and sometimes changing roles in determining the right amount. So let's dig in using examples for each of these factors to illustrate exactly how you can use them to find the perfect policy amount for your needs.

How to Choose a Life Insurance Amount Based on Your Income

Income is perhaps the simplest way to determine the amount for your life insurance. Most insurers recommend a policy that covers between six and 10 times your annual income. So, if you earn $50,000 annually, the recommended life insurance amount would be between $300,000 and $500,000.

This approach is maybe the easiest to calculate, and it accounts well for your current standard of living, which is typically based around your income. But it also has some important shortcomings:

- It doesn't account for inflation. While $500,000 might be ten times your annual income now, it probably won't be that when the policy comes due.

- It doesn't account for any outstanding debts. If you have none, it can work well. If you do, the policy might just be enough to pay those but offer little other benefits.

- It doesn't account for indirect expenses. For example, if a stay-at-home parent passes away, the amount would likely be low, but the remaining partner would need to cover new childcare expenses.

As a result, some financial planners simply recommend upping the amount to 10-15 times your annual income. For a more nuanced approach, consider taking other factors into account.

How Your Family and Living Situation Play Into the Ideal Life Insurance Amount

Let's discuss your family situation next. If you live on your own, this section is likely irrelevant to determine the ideal amount. But what if you have a spouse that relies on your income, and/or children that need to be taken care of in the event that you pass away?

One approach you can take in this case is the "income plus" method of getting life insurance. Use the same 6-10 times the annual income formula mentioned above, but add $100,000 for every dependent you have. It's a simple method that accounts for potential college and childcare expenses, making sure that your children are taken care of even in the unlikeliest of events.

If you live with a spouse, another popular method is for both of you to get life insurance. That approach ensures that if both of you are involved in the same accidents, the monetary amount multiplies for your children, ensuring that their needs can be taken care of.

It's still a relatively simplistic calculation, of course, because it doesn't include any consideration of your debts or your specific living situation. So, more comprehensive calculations should include those factors as part of the same process.

You may also like:

What is a Good Life Insurance Amount if I Have Debt?

From mortgages to car loans and other expenses, most people probably have at least some debts built into their monthly budget. These debts are easy to account for initially, but become problematic if a regular income goes away.

That's why some experts recommend determining the life insurance amount in your policy based on your debts.

The calculation for taking this approach is relatively simple:

- Add together all of your current debts, including your mortgage, car loans, credit cards, student loans, etc.

- Add about 10% to the full amount as a buffer to account for any potential interest or extra payoff rules.

- The result is the full life insurance amount you need for your beneficiaries to pay off all debts.

This approach tends to be more cautious than solely basing your life insurance on your income, but its shortcomings are also obvious. While your family might be left with enough money to pay off your debts, they won't have additional funds to account for regular living expenses. In other words, your current debt is a component of your life insurance but shouldn't be the only consideration.

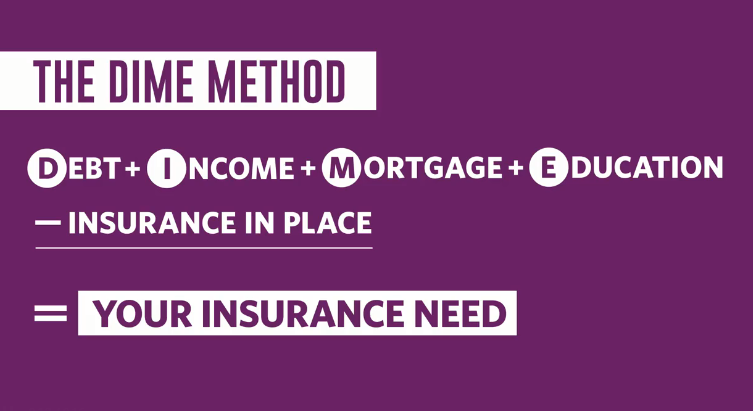

The DIME Method for Life Insurance Coverage

All the basic approaches above are pieces to the puzzle, but they don't paint the whole picture. That's because picking the right amount for your life insurance depends on too many factors to isolate any one of them. It's why especially independent financial planners tend to recommend what they call the DIME method. The acronym covers four components of a larger equation:

- Debt, making sure that any beneficiary gets enough funds to pay off all of your loan and credit card debts that aren't forgiven in the event of your passing.

- Income, based on how many years you believe your family needs to have your income replaced with life insurance coverage. Some experts recommend using the year your youngest child turns 18 as the end point for this calculation.

- Mortgage, pulled out from other debts because for homeowners, it's usually the biggest loan in your name.

- Education, especially as it relates to your children's college tuition, room, and board. Use resources like The College Board's Trends in College Pricing to determine how many funds you should calculate with.

All four of these variables add together for the most comprehensive recommended life insurance amount you could expect. Of course, that amount also tends to be high, making it difficult to afford depending on your age. That's what makes the last step so important: making sure that the amount is actually right for you and your current budget, as well.

5 Considerations to Make Sure the Right Life Insurance Amount is Right For You

Let's say that through DIME or another method, you have calculated what you believe is the perfect amount of life insurance for you to leave to your beneficiaries. Even with that amount, you still need to keep a few important things in mind:

- Keep your monthly budget in mind. If you cannot afford the monthly payment, it probably won't be the right policy for you.

- Understand the difference between term and whole life. Which of these types you choose will influence the amount you can afford.

- Keep future increases in mind. Your income will rise, but your standards of living might as well. Hopefully, your debts will go down. You can't predict the future, but you can build in some securities to have at least a good estimate of the cushion you'll need.

- Talk it through. A life insurance policy is not a decision that should be made in isolation. Have a chat with your spouse, and run through the numbers together. It also doesn't hurt to talk with others in your family who have life insurance policies to learn more about their approach.

- Talk to a financial advisor. When you're just not sure enough about your options or how life insurance will fit into your budget, allow a professional to help you. They can walk you through all the steps to make sure the amount you choose is right, not just in general or for your age group but for your individual situation.

With these variables in mind, one thing becomes clear: simply asking whether $250,000 or $500,000 in life insurance is enough misses the point. Instead, your goal should be to find a policy that works with your financial situation, your family needs, and your unique environment. It's the only way to make sure that the policy you end up with matches your needs and expectations.

Conclusion

Settling on the right life insurance policy is one of the bigger financial decisions you will make in life. That's especially true because the beneficiary will not be yourself, but those closest to you.

It's also what makes finding the right amount so important to your and your family's future. Rather than using a simplistic amount, working within a more complex method like DIME can make sure you consider all the variables involved. With the right idea of an amount in mind, you have everything you need to approach a life insurance provider about their options and plans.

You may also be interested in reading:

- 995 Colonial Penn Life Insurance Plan: Is it Really $9.95?

- MFTA Life Insurance: What Is it and Should You Get It?

Cheap Life Insurance Quotes by Age

The responses below are not provided, commissioned, reviewed, approved, or otherwise endorsed by any financial entity or advertiser. It is not the advertiser’s responsibility to ensure all posts and/or questions are answered.

![Can You Get Life Insurance for Your Parents? [Complete Guide]](/assets/images/4195a596c9c2e2afdae7712685f340fc.png)