Last Updated on: Jan 23, 2023

If you are in the position to pay off your mortgage early, it is best first to ask your lender if there are any prepayment penalty charges. Most mortgage lenders charge a prepayment penalty when borrowers pay off their loan balance before the final payment's due date. Depending on how long the loan has been out, this penalty can range between zero to two percent of the balance being paid off. The best way to avoid prepayment penalties is to have a better understanding of how these charges are applied and if they are legal.

What We'll Cover

- What is an Early Repayment Charge (ERC)?

- How Are These Early Repayment Charges Calculated?

- Can You Avoid Early Repayment Charges on Mortgages?

- Do All Mortgages Have an Early Repayment Charge?

- Top 8 Best Mortgage Deals with No Early Repayment Charges

- Is ERC Worth paying?

- Are Prepayment Penalties Allowed?

- Do I Need a Real Estate Attorney to Help with Getting a Mortgage?

- How to find out if Your Loan Has a Prepayment Penalty Clause

- Conclusion

You may also like: How Soon Can A Mortgage be Refinanced?

What is an Early Repayment Charge (ERC)?

An early repayment charge (also known as "Early Redemption Penalty") is a fee that some mortgage lenders charge when you pay off your loan (or even part of it) ahead of schedule.

And you may wonder: Why would I have to pay a penalty for paying my debt?...Well, here's the thing: since lenders make money through the interest they charge on loans to borrowers, when you decide to pay off your loan before the schedule term, it means less revenue the lender anticipated for the original time period of your loan. So, in order to them make up for the losses, they will charge you a prepayment penalty.

How Are These Early Repayment Charges Calculated?

Early repayment charges are sometimes a set fee; however, most of the time, it is calculated based on a percentage of the final balance of your mortgage. Some companies charge different rates based on how long you have had the loan because earlier in the loan; you tend to pay less toward the principal and the lender needs to recuperate some of the lost interest. Prepayment charges range between 0.5 percent and 4 percent of the final balance being paid off.

Can You Avoid Early Repayment Charges on Mortgages?

Some lending companies charge prepayment fees; however, they can easily be avoided doing the following:

- If you qualify, opt for an FHA or VA loan, which is not eligible for lenders to charge early repayment charges.

- Additionally, ways to avoid these unnecessary fees is to shop around and find a lender that does not charge prepayment fees on their loans.

- Finally, carefully read your mortgage loan agreement and ensure there is no hidden clause claiming the lender can charge you an early repayment fee. And if, by any chance, the lender you're interesting in use does charge an ERC, find out when and how the penalty kicks in so that you can stay within the parameters and avoid triggering a penalty.

It might also be possible to negotiate with the lender to waive these fees or reduce them when paying off your mortgage.

Do All Mortgages Have an Early Repayment Charge?

Not every mortgage contract has an early repayment charge attached to them. With a bit of research and comparison shopping, it is possible to find mortgage lenders who do not charge these fees. Federal law does prohibit prepayment penalties for some home loans, including FHA, VA, and USDA mortgage loans.

Below we've included a top pick with great options for you choose from

Top 8 Best Mortgage Deals with No Early Repayment Charges

Not every lender offers the same benefits, interest rates, and loan terms, so it is always best to shop around and learn everything you can about the various mortgage options available. Some of the best mortgage companies that do not charge early repayment fees include:

Axos Bank

Axos Bank offers various flexible mortgage loan options, including FHA, VA, and home equity lines of credit. Most of the mortgages provided through this bank do not have prepayment penalties. When applying for the loan, speak with the loan officer and ask for loans that do not charge these penalties.

See Related: Axos Bank Review [2024]

Lendingtree

Lendingtree does not charge mortgage prepayment penalties; however, some lending partners might. Tips to avoid paying prepayment charges through a Lendingtree lender may include negotiating with the lender to remove prepayment penalties from the loan and comparing all Lendingtree partner loans to find those that do not have this penalty attached to the mortgage loan.

Credible

Credible as a service does not charge mortgage prepayment penalties; however, some partner financial institutions may charge these penalties. Use Credible's assistance to find a finance company that offers single-family FHA loans, VA loans, USDA loans, or a loan with an adjustable rate. These loans are not subject to prepayment penalties.

Wells Fargo

Wells Fargo does not charge prepayment penalties and advises homebuyers to check the mortgage paperwork with other lenders to see if there is a "prepayment penalty" or "prepayment disclosure" section.

Stilt

Stilt is an online lender servicing the immigrant and noncitizen community in America, offering loans to people who may have trouble getting a mortgage through traditional means. Stilt does not charge any prepayment penalties on their mortgage loans.

Lending Club

LendingClub offers mortgages and personal loans with no prepayment penalties. This peer-to-peer lender provides many alternatives to help homebuyers find the perfect mortgage for their needs. Due to the high standards of this company, those who qualify for mortgages have excellent credit.

SoFi

SoFi is another online lender offering mortgage loans with no prepayment penalties; however, their loan requirements are strict, and most borrowers have an annual income of $100,000. This bank provides flexible terms and can find a mortgage to meet your unique needs.

You may want to read:

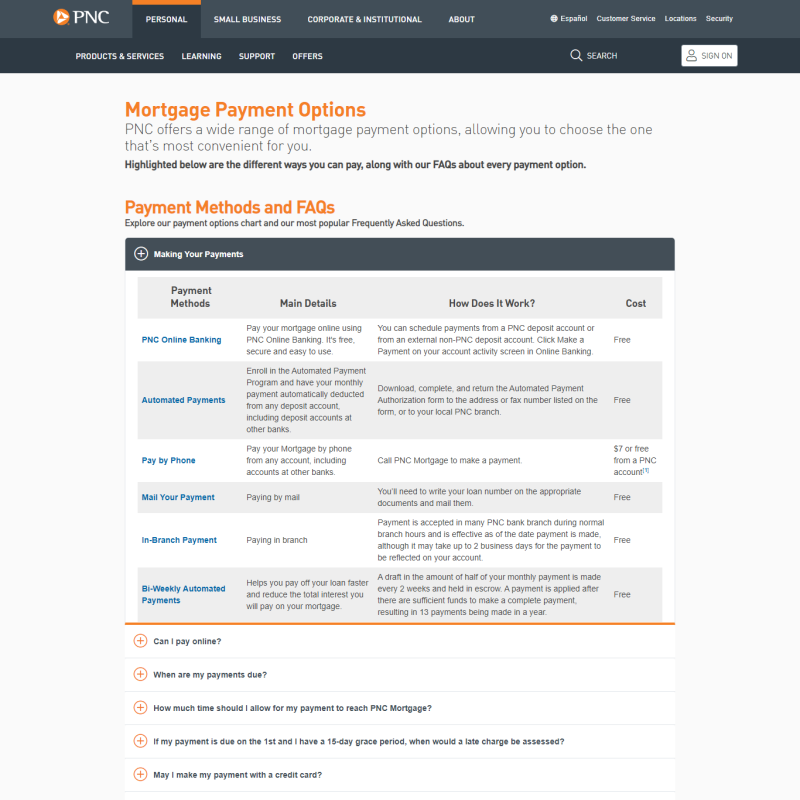

PNC Bank

PNC Bank offers mortgages with no prepayment penalties for homebuyers. When applying for a loan, ask for approval for a loan option with no prepayment penalties.

Is ERC Worth paying?

When you have enough money to pay off your mortgage, and there is a clause including early repayment charges, it is time to determine if these fees are worth paying.

Paying off your mortgage early with an ERC may still be less costly than if you were to continue paying on the loan and all of the associated interest. Before agreeing to pay off the early repayment charges, it is best to calculate if you will save money by paying it off with the charges. If you are not better off, it might be best to continue paying your mortgage as agreed upon when you established the loan contract.

If you are unsure if the ERC is worth paying, it might be best to speak with your mortgage adviser to learn more about your options and the benefits of paying the loan's balance before the final payment. A mortgage advisor can help determine if there are any early repayment charges associated with your loan and how much these fees will be. Additionally, hiring an attorney specializing in mortgage loans can help avoid singing a mortgage agreement with prepayment penalties and can help reduce these fees when you are ready to pay off your existing mortgage loan.

Are Prepayment Penalties Allowed?

For most modern-day mortgages, prepayment penalty charges are not allowed; however, there are some instances where these charges are still allowed. For FHA, USDA, and VA mortgage loans, prepayment penalties are not permitted. Additionally, it is best to speak with a mortgage advisor or attorney to determine if the early repayment penalties are legal and if there are any options to help you reduce or eliminate these charges when paying off your mortgage loan early.

Do I Need a Real Estate Attorney to Help with Getting a Mortgage?

When applying for a mortgage, hiring a real estate attorney is not necessary. However, it is very beneficial to hire an attorney to review your loan contract and purchase agreement. Additionally, a real estate attorney can help identify prepayment penalties in your mortgage agreement and determine if they are legal.

Even if prepayment penalties are allowed, there are several restrictions. For example, a prepayment penalty can only be charged within the first three years of the loan. After three years of payments, these charges are no longer allowed. Additionally, there are limits on how much the prepayment penalties can be. For example, for most loans that are less than two years, no more than two percent remaining balance is charged as part of this fee.

How to find out if Your Loan Has a Prepayment Penalty Clause

Speak with your mortgage counselor to learn more about your mortgage loan and if any prepayment penalties are included in the loan agreement. Your mortgage counselor can help determine if your loan agreement has prepayment penalty fees and how to avoid paying them. Ultimately, if early repayment fees are added to your mortgage loan, legally, there must be a clause that clearly states the fees and how charges are calculated.

Conclusion

When considering paying off your mortgage early, it is best to check to ensure you are not being penalized for early repayment of the loan. Additionally, if you are looking for a mortgage, look for one that offers no early repayment charge mortgage terms. Finally, if you are struggling to find mortgage deals with no early repayment charge attached to them, do some research or contact your local mortgage broker to learn more about mortgage repayment fees.

The responses below are not provided, commissioned, reviewed, approved, or otherwise endorsed by any financial entity or advertiser. It is not the advertiser’s responsibility to ensure all posts and/or questions are answered.