![Kentucky Mortgage Rates and Best Lenders [Updated 2023]](/assets/images/1be7c589e6bb1ecd611c19a04203444e.png)

Last Updated on: Jan 05, 2023

Homeownership is one of the most significant financial choices that many people make. For Kentucky residents, achieving this dream is much easier than for residents in other areas. This is because Kentucky is known for being one of the most affordable states when it comes to house prices. On top of the affordability of homes, the state government gives a tax credit accompanied by a homebuyer assistance program for first-time buyers. On average, the national median value for houses is $229,700. For Kentucky, however, the median house value stands at $148,000, a whopping $81,600 less than the national median.

What We'll Cover

This is why Kentucky's homeownership rate has consistently remained above the national rate. According to the United States Federal Reserve, the homeownership rate in Kentucky was 69.5% as of January 2019. That’s two percentage points higher than the present national homeownership rate of 67.4%.

As in many states, most homebuyers — especially first-time homebuyers — rely on mortgages to finance the purchase. Because of the state benefits and affordability, more and more Kentucky residents are taking up mortgage loans. According to the Consumer Financial Protection Bureau's Consumer Credit Panel, there was a 4% increase in new mortgages year-over-year as of April 2019.

Even with government incentives and a low average price for houses, taking a mortgage loan and buying a home is a substantial long-term commitment. It is essential for homebuyers to find the best mortgages lenders in Kentucky to access affordable KY mortgage rates.

With numerous mortgage lenders in Kentucky, it can be challenging to determine which one best suits your needs. In this article, you will learn all about Kentucky mortgage rates and find some of the best mortgages lenders in Kentucky.

KY Mortgage Rates

When shopping for mortgages, it's easy to get caught up with the idea of owning a home and settle for the first offer you get. However, finding the best Kentucky mortgage rates is just as important as finding a house that suits you. Think of it this way: even if you're looking for a three-bedroom home, you will come across some two and five-bedroom houses. Regardless of how good they are, they will not suit your needs.

With the smaller house, your family will not be comfortable, especially if it's big. While you may be able to afford the bigger house, it will cause financial strain down the line. The same goes for mortgage loans. Even if the best mortgage lenders in Kentucky offer rates that differ by one percent, it matters a lot. The compound effect of saving that one percent will save you thousands of dollars across the lifetime of your mortgage repayment period.

With Kentucky mortgage rates ranging from 2.5% to 3.5%, the average mortgage rate for a 30-year fixed rate is 2.87%, and the average rate for a 15-year fixed mortgage is 2.765%. The rate for a 5/1 adjustable-rate mortgage (ARM) is 2.95%.

Best Lenders and Brokers in Kentucky

Fortunately for the residents of the Bluegrass State, there are many Kentucky mortgage rates to choose from. However, this is also a challenge as it can be overwhelming to choose between Kentucky mortgage lenders. To make it easy for you, here's a list of some of the best mortgages lenders in Kentucky:

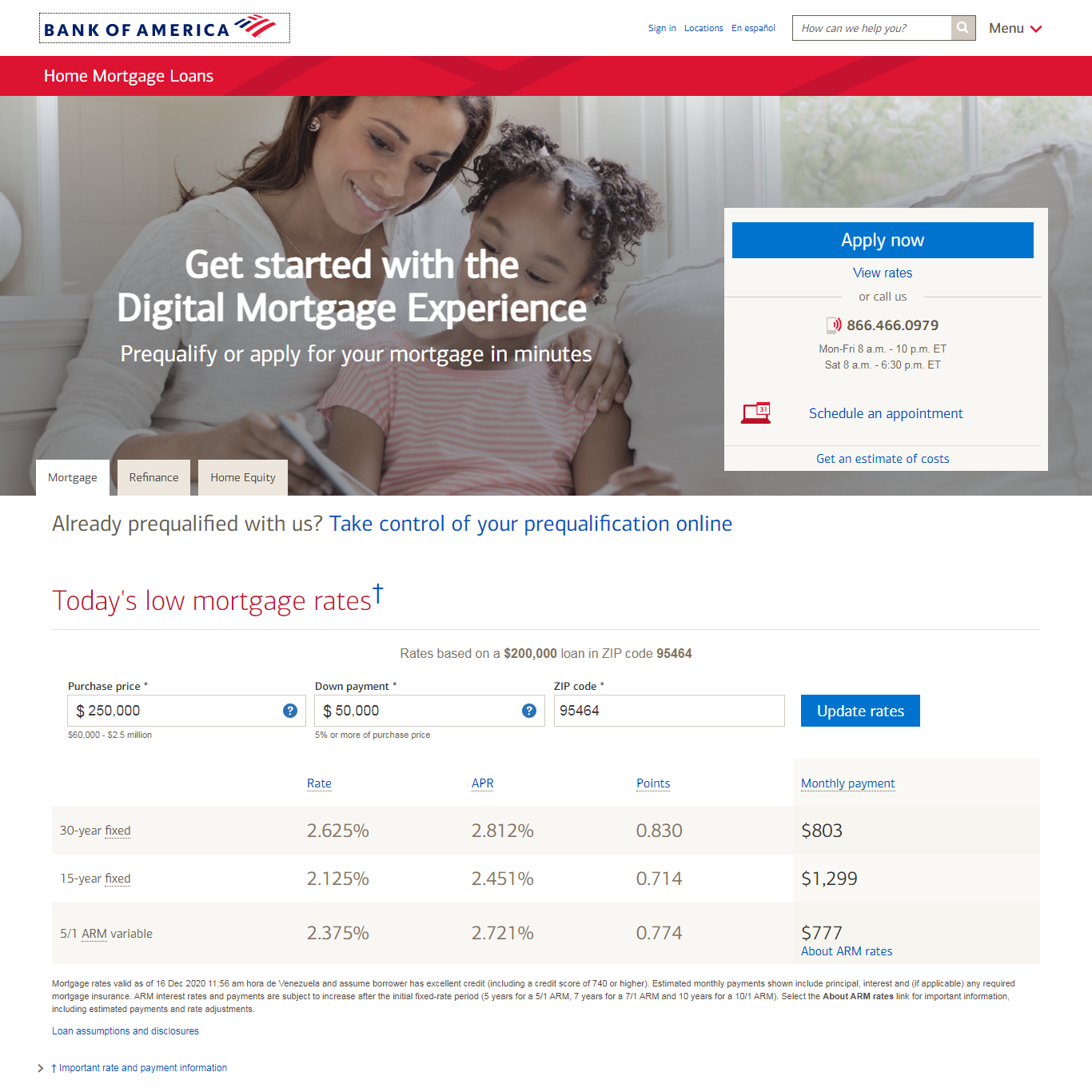

Bank of America

If you are a first-time homebuyer, Bank of America is arguably the best mortgage lender for you. Through their America's Home Grant® Program, you can access closing cost assistance of up to $7,500. Along with this program, Bank of America also offers mortgage types like home equity lines of credit, VA, and refinancing.

Compared to other lenders, they offer lower rates for 30-year fixed-rate loans. The maximum loan amount you can get is $5 million. However, you must have a FICO credit score of 600 and above to get a loan from the Bank of America.

Another feature that makes the Bank of America one of the best mortgage lenders in Kentucky is its A+ Better Business Bureau rating. Their services can be accessed through their branches in person or online via email and chat.

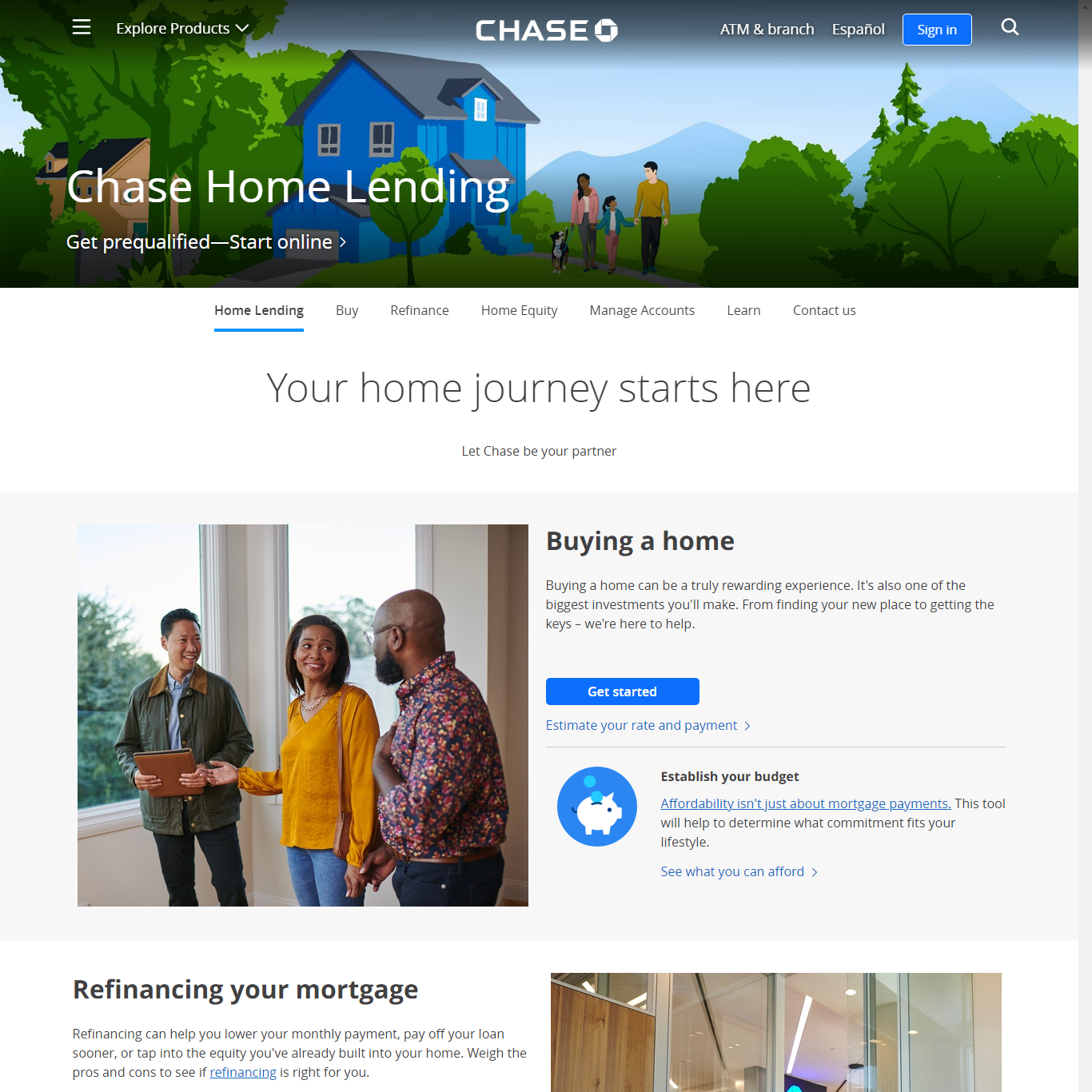

Chase

As one of the largest banks in the country, Chase is an ideal option for Kentucky residents in need of a mortgage loan. Some of the mortgage types offered by Chase bank include conventional mortgages, ARMs, FHA loans, VA loans, and refinances. Their biggest selling point is the low Kentucky mortgage rates they offer.

The maximum loan offered is $3 million. To qualify for a Chase mortgage loan, you need a FICO credit score of at least 620. They accept down payments of as low as 3% and have a Better Business Bureau rating of A+.

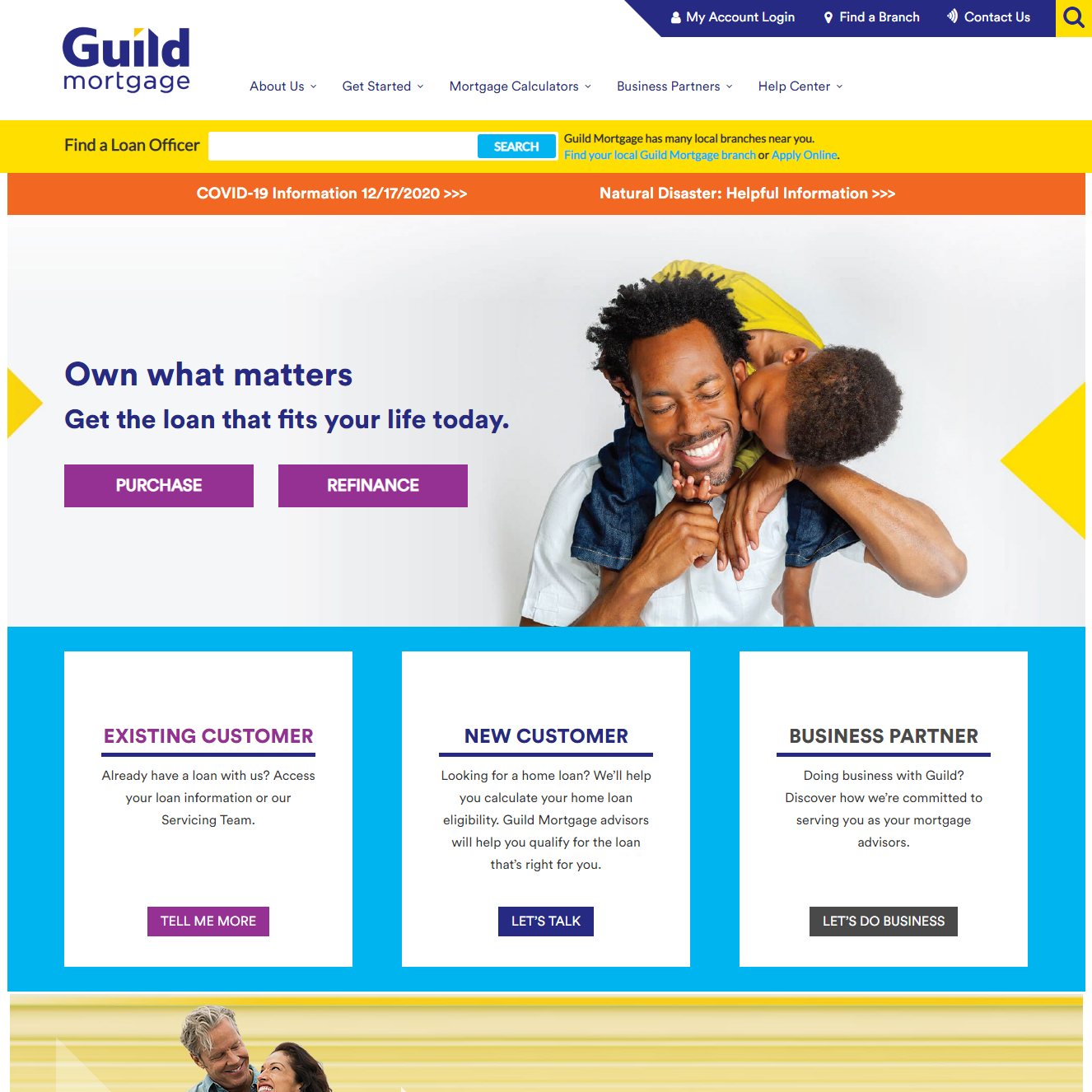

Guild Mortgage

Founded in 1960, Guild Mortgage is an institution focused on giving people quality home loans. With numerous loan products on offer, they are among the best mortgage lenders in Kentucky. Along with conventional loans and home equity loans, they also offer government-backed mortgages.

The maximum loan amount varies from one customer to the next. However, applicants need to have a FICO credit score of at least 600. As a first-time homebuyer, you will benefit from special mortgage programs.

Purchase or Refinance

Access to the best Kentucky mortgage rates allows many people to become homeowners. However, even if you already have a mortgage plan and the rates are not ideal, there's still a solution. Through mortgage refinancing, you can pay off your existing mortgage loan and replace it with one that has lower rates.

Along with accessing lower KY mortgage rates, you can refinance your mortgage to:

- Reduce your mortgage repayment period

- Convert a fixed-mortgage rate to an adjustable-rate mortgage (ARM) or vice versa

- Utilize your home equity to finance a large purchase, consolidate debt, or deal with a financial emergency

Just as with a regular mortgage, a title search and appraisal must be conducted for a refinancing. This can cost anywhere from 2-5% of the original mortgage in Kentucky.

KY FHA Loans

There are many homebuyer assistance programs and a tax credit administered by the Kentucky Housing Corporation (KHC) available in the state. Those options include:

KHC Preferred Risk Program

The KHC Preferred Risk Program is one of the FHA products available for Kentucky residents. It offers a 30-year conventional loan that does not require private mortgage insurance (PMI), and the down payments are as low as 3%. When it comes to borrower contributions and reserves, there is no minimum requirement. Borrowers who qualify for the KHC Preferred Risk Program can also combine it with KHC's down payment assistance programs.

The requirements to qualify for this loan include:

- A minimum credit score of 660

- Have a maximum loan-to-value ratio (LTV) of 97%

- Be 80% below the area median income (AMI)

KHC Preferred Program

KHC's Preferred Program is similar to the Preferred Risk Program. It requires a 3% down payment, but it also requires mortgage insurance. Other than completing a homebuyer education program, borrowers must also have:

- A minimum credit score of 660

- A maximum LTV of 97%

KHC Preferred Plus 80

If you earn between 80 and 100 percent of the county limits, you can qualify for the KHC Preferred Plus 80 mortgage. With this product, all the requirements are the same as the KHC Preferred Program, except for the differing income requirements.

Down Payment Assistance Programs (DAP)

Under the Down Payment Assistance Programs, you have two options:

- Regular DAP: In this program, mortgage loan repayments are made over a five-year period at a rate of 5.5%. You can access a loan of up to $6,000 that can be used for the down payment and closing costs of a house. This product does not require borrowers to have a cash reserve or liquid asset review. However, the Affordable DAP's purchase price limit is applicable.

- Affordable DAP: This is a low-cost loan that can be used to cover the down payment and closing costs of a house. The maximum amount available is $6,000 for a period of 10 years at a rate of 1%. As of August 2020, the home purchase price limit is $327,334, and borrowers must also meet the county's income requirements.

Mortgage Credit Certificate and Kentucky Homebuyer Tax Credit

If you qualify for FHA products, you may also be eligible for a tax credit, or mortgage credit certificate. With a mortgage credit certificate (MCC), the amount you will be required to pay in federal taxes will reduce over each year you occupy your house.

Up to 25% of your annual mortgage interest can be deducted for your tax credit. However, there's a limit of $2,000. Depending on where you live and the number of people in your household, there are income limits and a purchase price cap of $294,600.

Bottom Line

If you’re a prospective homeowner, there's no better place than Kentucky. There are many mortgage lenders to choose from. With some effort on your part and patience to search for the best mortgage lenders in Kentucky, you can get the best rates in the state. However, it does not have to be tedious. Click here to find a detailed breakdown of the best mortgage lenders in Kentucky.

The responses below are not provided, commissioned, reviewed, approved, or otherwise endorsed by any financial entity or advertiser. It is not the advertiser’s responsibility to ensure all posts and/or questions are answered.